Corporate tax registration for non-resident investors in the UAE is a mandatory legal obligation once specific conditions are met, including establishing a taxable presence or generating UAE-source income. Corporate Tax Registration in the UAE must be carefully assessed to ensure compliance with applicable legal thresholds and regulatory triggers. Failure to assess these obligations may result in penalties exceeding AED 10,000 and potential disruption of business operations. Under Federal Decree-Law No. 47 on the Taxation of Corporations and Businesses, non-resident investors who incur tax liability must comply with all registration and filing requirements. This guide outlines the framework to evaluate your corporate tax position, identify mandatory registration triggers, and complete the process to ensure full regulatory compliance as a non-resident operating within the UAE’s business environment.

Overview of UAE Corporate Tax and Its Applicability to Non-Resident Investors

The UAE enforces a federal corporate tax regime on business profits, applying a standard rate of 9% on taxable income exceeding AED 375,000. Governed by Federal Decree-Law No. 47, this regime applies equally to resident and non-resident investors generating UAE-source income or maintaining a taxable presence within the country.

Non-resident investors are required to conduct a detailed assessment of their business activities, contract arrangements, and commercial relationships within the UAE. The regulatory authority targets foreign entities and individuals that exert significant control, realize profits, or manage economic activities on UAE territory or through UAE-linked assets.

Errors in determining tax applicability or missing registration deadlines expose entities to substantial financial penalties and restricted operational capabilities. Understanding the provisions detailed in A Detailed Summary of UAE Corporate Tax Federal Decree Law is essential for effective risk management and maintaining continuous legal compliance as a non-resident business participant.

Who is Considered a Non-Resident Investor Under UAE Corporate Tax?

Non-resident status under UAE corporate tax focuses on residency criteria, taxable presence, and income source location. Non-resident investors comprise foreign companies, partnerships, or individuals who do not establish UAE residency but conduct taxable activities or generate income within the UAE jurisdiction.

Critical determinants, such as maintaining a Permanent Establishment or receiving UAE-sourced income, subject entities or individuals to the regulatory framework. Misinterpreting these definitions increases the risk of unreported liabilities and potential penalties under local tax laws. Consulting FTA Corporate Tax Rules for Non-Resident Persons enables accurate classification and proper tax positioning.

Definition of a Non-Resident Person

A non-resident person under UAE law is any entity or individual who does not satisfy UAE tax residency criteria but earns income from UAE sources or maintains a taxable business presence, such as a Permanent Establishment.

Tax Liability Triggers: Permanent Establishment and UAE-Sourced Income

Non-residents incur corporate tax liability when they establish a permanent establishment or derive income taxable under UAE corporate tax legislation.

- Permanent Establishment includes physical or economic presence in the UAE: An office, branch, or agent acting on behalf of a foreign entity constitutes a taxable presence.

- Income from UAE contracts or assets triggers liability: Earnings from services, sales, or rentals conducted within the UAE are subject to corporate tax.

- Business activities conducted within the UAE create a nexus: Engaging in trade or business through fixed or virtual platforms establishes tax obligations.

- Active management of assets in the UAE: Direct oversight or administration of assets located in the UAE may establish taxable presence.

Common Examples of Non-Resident Investors

Typical scenarios involve foreign entities engaged with UAE businesses or assets meeting thresholds requiring tax registration.

- Foreign company with sales representative in the UAE: Employing or contracting representatives within the UAE triggers taxable status.

- Overseas consultancy providing services to UAE clients : Revenue from advisory or management services rendered to UAE-based clients is subject to corporate tax.

- Holding company owning or leasing property in the UAE : Ownership or leasing of real estate in the UAE creates corporate tax liability.

- Foreign entity managing a UAE project remotely : Even remote project oversight may constitute a permanent establishment if significant UAE activities occur.

When is Corporate Tax Registration Mandatory for Non-Residents?

Corporate tax registration becomes obligatory for non-resident investors upon specific regulatory triggers defined by the Federal Tax Authority. These include the formation of a permanent establishment, exceeding taxable income thresholds, or surpassing business turnover limits within the UAE.

Non-compliance with registration deadlines carries substantial fines and damages reputation. Non-residents should consult Corporate Tax Registration in UAE: A Comprehensive Guide to understand registration timing, criteria, and relevant Qualifying Income for Freezone Persons under UAE Corporate Tax exemptions.

Corporate Tax Registration Triggers

Registration is mandated by specific threshold events and income levels stipulated in the regulations.

- Having a Permanent Establishment in the UAE : Any fixed or representative presence, irrespective of incorporation, necessitates tax registration.

- Earning taxable income exceeding AED 375,000 : Non-resident entities exceeding this threshold must register regardless of their operational base.

- Natural persons with business turnover over AED 1 million : Individuals conducting commercial activities above this turnover are required to register.

- Provision of continuous services to UAE customers : Ongoing services such as consultancy or management spanning multiple financial periods may trigger registration.

- Holding income-generating assets in the UAE: Revenue from property, intellectual property, or investments within the UAE mandates registration.

Registration Deadlines and Compliance Timelines

When a registration obligation arises, non-resident investors are required to register with the FTA within the legally specified timeframe. Late registration can lead to fines under UAE regulations and may disrupt business continuity.

Exceptions and Exemptions from Registration

Certain entities and income categories are exempt from corporate tax registration upon meeting specific FTA conditions and qualifying criteria.

- Qualifying Free Zone entities with 0% tax rate: Entities that satisfy the FTA's 'qualifying income' conditions benefit from exemption, yet must notify or complete simplified registration.

- International transportation income exemptions : Income from cross-border shipping and transportation may be excluded under applicable treaties.

- Other exempt income categories per FTA guidelines : Passive income streams, such as returns on government bonds or certain dividends, may qualify for exemption.

- Sovereign and government-owned companies: Certain government bodies and investment funds are statutorily exempt from registration.

- Income from wholly foreign activities: Revenue earned exclusively outside the UAE with no taxable local presence generally falls outside the corporate tax scope.

| Condition | Threshold/Requirement | Deadline/Notes |

|---|---|---|

| Permanent Establishment in UAE | Any taxable presence | Non-residents must register within 6 months of the Permanent Establishment (PE) being established |

| Taxable UAE Income | The AED 375,000 is the threshold for paying tax, not for the obligation to register. | Non-resident entities with a PE must register regardless of the income level. |

| Natural Person Business Turnover | Over AED 1 million turnover | Mandatory registration required |

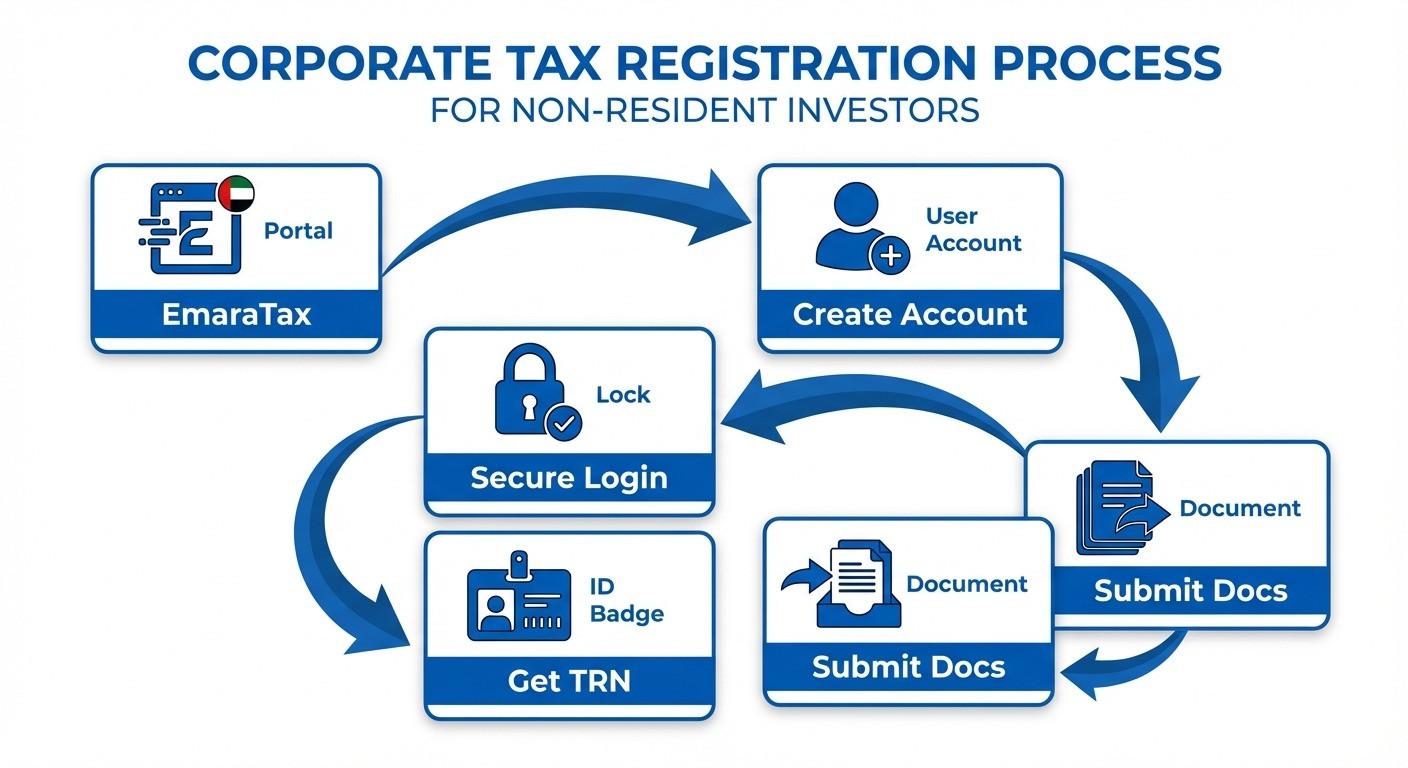

Corporate Tax Registration Process for Non-Resident Investors

Non-resident investors must follow the prescribed steps to register with the Federal Tax Authority via the EmaraTax portal. Timely submission of accurate documentation and disclosure is essential. Each stage aligns with the FTA’s risk management policies and statutory reporting obligations.

Detailed instructions are available in How to Register for Corporate Tax in the UAE? | Step-by-Step Guide to ensure precision throughout the process.

Accessing the EmaraTax Portal

Registration must be completed through the official EmaraTax digital platform, utilizing proper authentication and navigation.

- Create an account on the EmaraTax portal: This is the initial step for all tax filings and communications.

- Ensure secure login with UAE Pass or credentials: Robust authentication safeguards data privacy and access.

- Navigate to the Corporate Tax registration section: Selecting the correct section prevents misfiling and processing delays.

Required Documentation for Registration

Registration requires submission of comprehensive business documentation, including commercial licenses, ownership evidence, valid identification, and proof of UAE-source income or presence. Proper documentation complies with FTA due diligence and expedites approval.

Obtaining the Tax Registration Number (TRN)

The FTA issues a unique TRN upon successful registration, which is essential for all tax filings and audits.

- TRN is mandatory for filing tax returns: Entities must use their TRN for all statutory submissions.

- Must be retained for audits and compliance: TRNs are verified during FTA investigations.

- Provides official recognition of tax status: The TRN legitimizes your tax obligations and eligibility to operate in the UAE.

Common Errors to Avoid During Registration

Avoiding errors during registration prevents fines and delays in tax processing.

- Incomplete or inconsistent business details: Missing or conflicting information leads to application rejections.

- Failure to declare permanent establishment : Concealment of UAE presence results in compliance violations.

- Missing or incorrect ownership information: Errors prompt FTA inquiries and suspend processing.

- Inaccurate entry of contact or business address: Discrepancies impede communications on registration status.

Common Challenges and Compliance Risks for Non-Resident Investors

Non-resident investors often encounter misunderstandings regarding permanent establishment rules, omissions in registration, and inaccuracies in filings. These issues increase the probability of audits and financial sanctions from the Authority.

Prompt actions supported by continuous advisory services are critical to avoid escalating penalties and maintain operational stability. Awareness of Corporate Tax fines in UAE: Be Aware Of The Penalties and UAE Corporate Tax Fines and Penalties fosters a proactive compliance approach.

Risks of Late or Incorrect Registration

Failing to register within deadlines or providing inaccurate information incurs significant legal and financial consequences.

- Monetary fines imposed by FTA: Late or erroneous registration results in fines starting from AED 10,000.

- Potential legal actions and reputational harm : Non-compliance may lead to judicial proceedings and blacklisting.

- Increased scrutiny in subsequent audits: Compliance failures result in intensified FTA audit frequency.

- Restricted access to UAE business opportunities : Regulatory non-compliance can delay or prevent new licenses and contractual agreements.

Misinterpretation of Permanent Establishment Rules

An incomplete understanding of permanent establishment criteria may cause underreporting of liabilities. Complex corporate arrangements require assessment against legal and economic substance standards to limit unintentional tax exposure.

Importance of Accurate and Timely Disclosures

Consistent and precise reporting to the FTA, including timely filing of corporate tax returns and business updates, ensures regulatory compliance.

- Regular filing of corporate tax returns: Meeting deadlines avoids statutory penalties.

- Updating FTA with business changes : Notifying structural or ownership changes maintains continuous compliance.

- Consulting tax professionals for guidance : Expert advice reduces errors and maximizes opportunities for lawful tax optimization.

Benefits of Professional Tax Advisory Services

Corporate Tax Advisory Services provide structured guidance to non-residents, lowering compliance risks, ensuring accurate registration, and delivering strategic planning for optimized legal and financial results.

Conclusion

Non-resident investors must continuously evaluate their corporate tax obligations in the UAE, focusing on permanent establishment criteria and UAE-sourced income. Proactive corporate tax registration, accurate documentation, and comprehensive reporting are essential to minimizing risk and maintaining uninterrupted business operations.

Selecting the right partner for ongoing compliance and advisory delivers sustained value beyond mere regulatory fulfillment. Considering the stringent FTA penalties for non-compliance, timely and precise professional support is indispensable.

By selecting Reyson Badger, you obtain a trusted advisor offering a client-centric approach, deep regulatory expertise, and a proven record of timely, transparent service delivery. We are dedicated to providing your business with customized, strategic guidance to achieve and sustain compliance within the UAE.

Frequently Asked Questions(FAQs)

1. Who is considered a non-resident person under the UAE Corporate Tax Law ?

A non-resident person is any individual, company, or entity that does not meet UAE tax residency criteria but has a permanent establishment or derives UAE-sourced income, thereby incurring liability under Federal Decree-Law No. 47.

2. When must a non-resident register for corporate tax in the UAE?

Registration is required when a non-resident establishes a permanent establishment, earns UAE-sourced income exceeding AED 375,000, or operates as a natural person with business turnover exceeding AED 1 million.

3. What triggers corporate tax liability for non-residents in the UAE?

Corporate tax liability arises from maintaining a permanent establishment, conducting taxable business activities, or deriving income from UAE sources as defined in the regulations.

4. What are the corporate tax rates applicable to non-resident persons?

Non-resident persons are subject to a standard 9% corporate tax on taxable income exceeding AED 375,000 pursuant to Federal Tax Authority regulations.

5. What are the penalties for non-compliance with UAE corporate tax laws?

Penalties include fines beginning at AED 10,000 for late registration, inaccurate filings, or failure to disclose business activities as mandated by the FTA.