Top 20 Corporate Tax Consultants in UAE

19-Jan-2026

Free Zone Corporate Tax in UAE

The United Arab Emirates (UAE) has proven to be one of the leading business destinations. Its good uae freezone corporate tax regime has helped in this. The freezone corporate tax in UAE has evolved significantly in the last few years with the introduction of a federal corporate tax regime in 2023. Against this backdrop, the Free Zones of the UAE have emerged as a critical component of the country's economic framework. They offer businesses a unique set of benefits that are not available elsewhere, such as tax exemptions, streamlined regulations, and world-class infrastructure. This overview will go into depth on the intricacies of the UAE's freezone corporate tax system, focusing on the critical role that Free Zones play in economic growth and foreign investment.

The framework governing the Free Zone Corporate Tax regime has been updated. This guide is current based on Ministerial Decision No. 229 of 2025 (Qualifying & Excluded Activities) and Decision No. 230 of 2025 (Recognised Price Reporting Agencies), which replace the prior MD 265 of 2023.

Here is the latest update on UAE Corporate Tax for Freezones

What are Free Zones in the UAE?

Free Zones in UAE are geographic areas designated with special regulatory and economic privileges given to businesses to attract foreign investment and promote economic diversification. The zones function according to their rules and regulations, which vary from those applied to businesses operating outside the zones. Major free zone functions include:

- Foreign Direct Investment (FDI) Attraction: Free zones try to attract international businesses by providing incentives such as tax exemptions and 100% foreign ownership.

- Ease of Trade: Free zones simplify the customs procedures that make importation and exportation easier, hence increasing the efficiency of trade.

- Economic Diversification: Free zones are promoting various industries, thus contributing to the overall aim of the UAE to diversify its economy away from reliance on oil revenues.

What is the Free Zone Corporate Tax Regime in UAE?

In the UAE, a free zone person refers to businesses that are set up and operated within one of the country's designated free zones. These businesses enjoy special tax breaks and regulatory advantages designed to attract foreign investment. With the introduction of UAE corporate tax in free zone areas, it's essential for both individual business owners and companies to understand how the new rules apply to their operations.

Natural Person

A natural person is a natural person in the UAE corporate tax context, who has business activities and generates business income. These persons may have to pay corporate tax as well if their business income crosses a particular threshold. More specifically, business income by a natural person exceeding AED 1 million must be subjected to corporate tax, whereas employment or investment income, not requiring any license, are not within the purview of tax.

Juridical Person

A juridical person is a legal entity which may be a corporation, partnership or limited liability company, recognised by law as having rights and obligations. All juridical persons in the UAE are liable to corporate tax on their taxable income, comprising profits arising from business carried out within the country.

What is Tax Applicability for Various Types of Entities?

The UAE corporate tax is applicable to different types of entities:

- Mainland Companies: All businesses incorporated in the UAE are subject to corporate tax on their worldwide income.

- Free Zone Companies: Qualifying free zone entities can benefit from a 0% corporate tax rate on certain types of income derived from eligible activities. However, under the framework of UAE corporate tax in free zone, these entities must adhere to specific regulatory requirements to maintain this preferential status.

- Foreign Companies with Permanent Establishments (PEs): Business entities of foreign entities operating through a PE in the UAE would be liable to corporate tax for income accruing from such activities.

- Individuals with Commercial Licenses: The persons carrying on business under commercial license, either as proprietor or freelancer, would be liable to corporate tax also.

What are the Special Tax Rules for FreeZone Companies?

Special provisions under the UAE corporate tax regime have been provided for the free zone companies :

- 0% Corporate Tax Rate: Qualifying free zone entities can benefit from a 0% tax rate on income derived from specific eligible activities. This is especially advantageous for businesses engaged in international trade or services.

- Regulatory Compliance: To maintain their tax-exempt status, free zone companies must comply with economic substance regulations and ensure that their activities align with those permitted within their respective free zones.

- Non-Qualifying Income: Any income not derived from qualifying activities may be subject to the standard 9% corporate tax rate applicable to other businesses.

Corporate Tax: Mainland vs Free Zones

The UAE applies different corporate tax rules for Mainland and Free Zone businesses. Here are the major differences :

| Category | Mainland | Free Zones |

|---|---|---|

| Corporate Tax Rates | A 9% tax rate is applied to any income above AED 375,000. | Many Free Zone businesses are tax-free on "Qualifying Income" by meeting certain criteria. |

| Tax on Qualifying Income | Any income above AED 375,000 is taxed at the standard rate. | Likely exempted from tax on income generated from activities aligned with Free Zone objectives. |

| Activities Eligible for Tax Benefits | Can carry out activities anywhere in the UAE with no restriction. | Tax benefits apply to specific activities; non-permitted activities may be taxed at normal rates. |

| Trading Restrictions | Can carry out activities anywhere in the UAE with no restriction. | May face restrictions in Mainland trade; often need a local distributor or branch for Mainland sales. |

| Tax Compliance | Must follow FTA regulations; proper registration and auditing procedures are mandatory. | Must also follow FTA regulations; requirements are slightly easier if tax exemptions apply. |

Find out more by reading A Quick Guide to Corporate Tax on Mainland and Free Zones

Qualifying Free zone Person

Who Can Be a Qualifying Free Zone Person?

A Qualifying Free Zone Person is a business entity that has met certain criteria stipulated by the UAE Corporate Tax Law . For this to be so, the business entity must meet six essential conditions:

6 Conditions for Qualifying Free Zone Persons

- Adequate Substance: The entity must ensure a minimum level of operating presences in the United Arab Emirates, which implies to have physical office spaces, employees, and being actually involved in business.

- Source of Qualifying Income: Business shall earn income that qualifies by meeting the criteria as given under the Cabinet's definition made in Cabinet Decision No. 55 of 2023.

- No Choice for Standard Corporate Tax: The entity must not have exercised its option to be subject to the standard corporate tax regime under the UAE Corporate Tax Law.

- Compliance with Transfer Pricing Rules: The QFZP must adhere to the Arm's Length Principle and maintain proper transfer pricing documentation as required by law.

- Economic Substance Regulations (ESR) : The business must carry out substantial economic activity within the Free Zone, proving its contribution to the UAE economy.

- No Excluded Activities: The entity must not engage in activities that are explicitly excluded from qualifying for the 0% corporate tax rate.

Understanding Qualifying Income

Qualifying Income denotes income that a Qualifying Free Zone Person derives from particular sources of activities that are eligible for a 0% corporate tax rate within the UAE Corporate Tax Law. This income is sourced through transactions and activities conducted within, or from, designated free zones.

Qualifying Income for Free Zone Persons

Qualifying income for free zone persons relates to:

- Exported from the UAE: Income accrued from exporting goods outside the UAE.

- Income from Other Free Zone Persons: Income earned through sales or services rendered to other businesses within the same or different Free Zones.

- Particular Services: Services of specified types that fall under activities eligible for qualification by the Cabinet. These include manufacturing, processing, and trading of qualified goods.

Examples of What Constitute Qualifying Income and Non-Qualifying Income

Qualifying Income Examples

- Sales to international customers where goods are shipped directly from the Free Zone.

- Revenue from providing logistics services to other Free Zone entities.

- Income from exploitation of intellectual property rights if it qualifies.

Non-Qualifying Income Examples

- Income from activities carried out in mainland UAE.

- Revenue from domestic sales within the UAE that do not qualify.

- Earnings from investments in non-qualifying assets or properties outside the Free Zone.

Qualifying Activities and Non-Qualifying Activities

Qualifying Activities and Non-Qualifying Activities in UAE Free Zones

Conditions for Qualifying for the 0% Tax Rate

Free Zone entities that meet the conditions of a Qualifying Free Zone Person (QFZP) can benefit from a 0% Corporate Tax rate. Qualifying income includes activities such as manufacturing, distribution in or from Designated Zones, and certain treasury or financing services. Income from mainland operations, excluded activities, or related-party transactions that exceed the de minimis threshold is subject to 9%.

- Adequate Substance: The business must maintain a physical presence in the Free Zone, including office space and employees.

- Qualifying Income: Revenue must originate from activities specifically designated as qualifying under the UAE Corporate Tax Law.

- No Election for Standard Corporate Tax: The entity must not opt to be taxed under the standard corporate tax regime.

- Compliance with Transfer Pricing Rules: The business must adhere to transfer pricing regulations to ensure transactions are conducted at arm's length.

- Economic Substance Regulations: The business must exhibit a significant level of economic activity in the Free Zone.

- No Engagement in Excluded Activities: The business must not conduct activities that are explicitly excluded from qualifying for the 0% tax rate.

Taxation of Non-Qualifying Activities Within Free Zones

Non-qualifying activities conducted by QFZPs are subject to the standard corporate tax rate of 9%. Any income derived from these activities will not benefit from the 0% rate, potentially impacting the overall tax liability of the business.

Excluded Activities

Certain activities are explicitly excluded from qualifying for the 0% corporate tax rate, including:

- Leasing Real Estate in Mainland UAE: Any income generated from leasing properties located outside the Free Zone.

- Banking and Insurance Services: Financial services that do not qualify under the Free Zone tax regime.

- Investment Income : Earnings from investments that do not meet qualifying criteria.

- Activities Involving Domestic Sales: Sales made to customers within mainland UAE that do not meet qualifying income definitions.

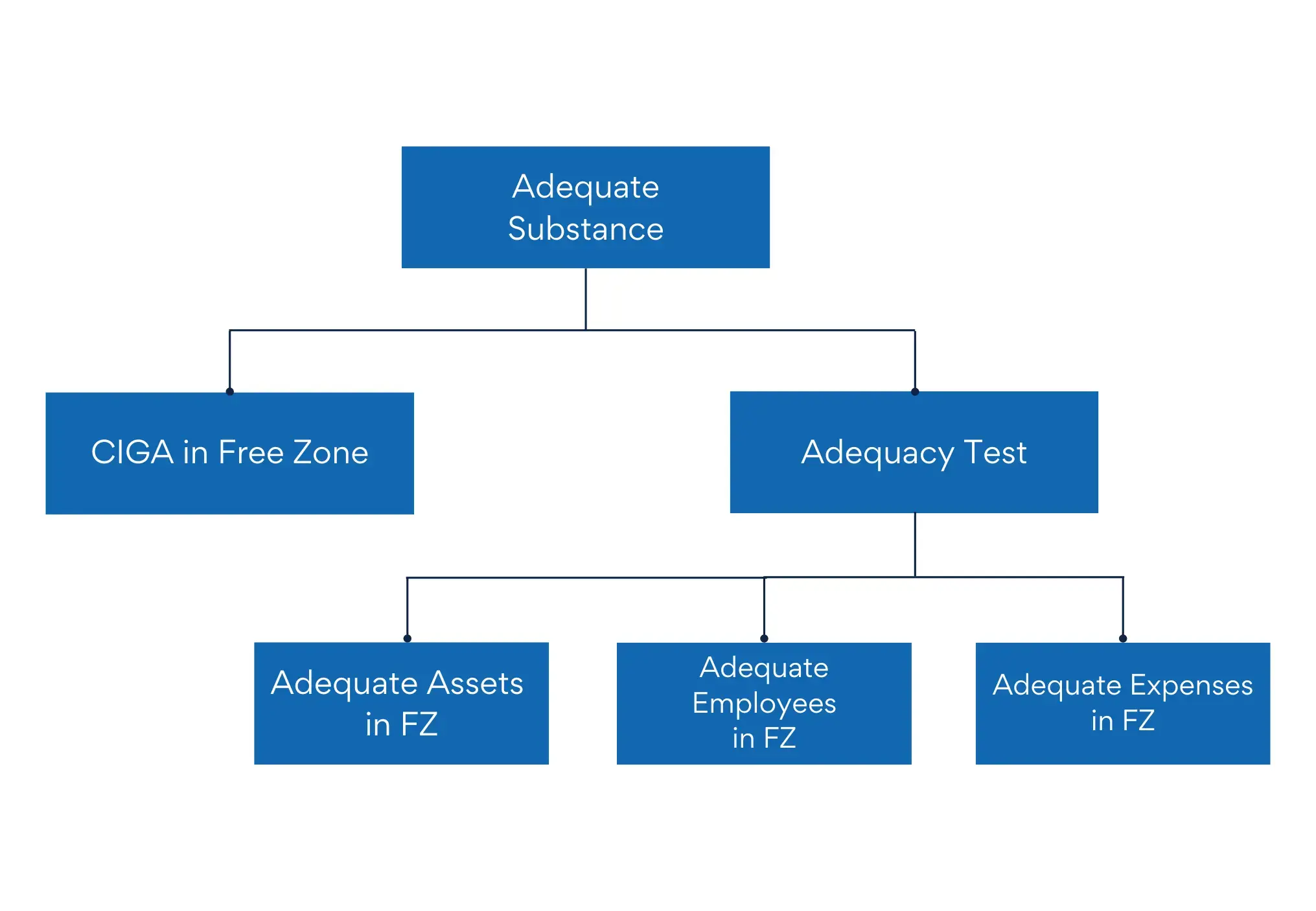

Adequate Substance

For having Adequate Substance in UAE, two regulations needs to be followed

- CIGA in Free Zone: Core income-generating activities (CIGA) must be carried out within the Free Zone.

- Adequacy Test: Businesses must meet requirements for having adequate assets, a sufficient number of qualified employees, and appropriate operating expenses relative to their activities.

Outsourcing Activities

Outsourcing Activities can be outsourced to a related party or a third party within the Free Zone, provided the Qualifying Free Zone Person maintains adequate supervision over the outsourced activities.

What is the De Minimis Requirement?

As permitted under the UAE freezone Corporate Tax Law and De Minimis requirement , Qualifying Free Zone persons may retain their 0 percent corporate tax on qualifying income should they have non-qualifying income; however their non-qualifying amount needs to be less than five percent of total revenue. Otherwise, their non-qualifying amount will be 5 million AED, or whatever is smaller.

Why is the De Minimis Requirement Important?

This requirement is intended to:

- Support Free Zone Operations: Allow businesses to operate in Free Zones but permit some income from other sources.

- Promote Compliance: Ensure companies comply with the UAE's corporate tax but benefit from a relatively friendly tax regime.

- Maintain Eligibility: Permit companies with minimal non-qualifying income to remain eligible for the 0% tax incentive.

If a Free Zone Person fails any QFZP condition or earns excessive non-qualifying income (above the de minimis limit), it loses 0% eligibility and is taxed at 9% for that and subsequent tax periods.

How Does the De Minimis Requirement Work?

Thresholds: The AED 5 million or 5% of total revenue whichever comes first, is the threshold of non-qualifying income for a QFZP.

Excluded from the calculation are:

Revenues from immovable properties in the Free Zone.

Incomes from permanent homes and establishments in the territory or abroad.

De-minimis Requirement

If a qualifying freezone person's non-qualifying income during a tax period does not surpass 5% of their total income for that tax period, or AED 5,000,000 (5 million dh), (whichever is lower), then the de-minimis requirement will be satisfied.

| Example 1 | Example 2 | |

|---|---|---|

| Total Revenue | 1,20,000,000 | 80,000,000 |

| 5% of Total Revenue | 6,000,000 | 4,000,000 |

| Threshold | 5,000,000 | 5,000,000 |

| Satisfies for De-Minimis Requirement | No | Yes |

To calculate the 5% in De-Minimis Requirement

(Non-Qualifying Income ÷ Total Income) × 100

What is Free Zone Corporate Tax in UAE?

Free Zone Corporate Tax, is the tax levied by the Free Zone system that distinguishes between earnings of qualifying and non-qualifying income for Free Zone Business

- 0% Rate: Applies to QFZPs on their qualifying income, if particular conditions are fulfilled.

- 9% Rate: Applied on taxable income which does not qualify under the Free Zone provisions or exceeds De Minimis thresholds.

Tax Rates and Thresholds

- Qualifying Income: This refers to income earned by businesses that benefits from a 0% corporate tax rate. There's also a threshold - any qualifying income up to AED 375,000 is exempt from tax.

- Non-Qualifying Income: This income is subject to the standard corporate tax rate of 9%. It applies to income exceeding the AED 375,000 threshold or income derived from activities not classified as qualifying.

- Special Rates for Large Multinationals: There are additional considerations for multinational corporations (MNCs) with very high global revenues. These companies may be subject to a different tax rate under the Organisation for Economic Co-operation and Development's (OECD's) Base Erosion and Profit Shifting (BEPS) 2.0 framework.

This system creates a competitive tax environment, particularly for small and medium businesses, by offering a tax-exempt zone for a portion of their profits.

What is the Taxation Process for Free Zone Entities in the UAE?

Free Zone companies must register for corporate tax through the Federal Tax Authority (FTA) using the EmaraTax online portal. The steps are involved in the process:

- Assess Business Activity: Companies should determine their income sources to identify qualifying income and segregate it from any mainland activities.

- Maintain Documentation and Records: Businesses must maintain detailed financial records, including audited statements if they have qualifying income, to support their tax filings.

- Register on the FTA Portal: Free Zone businesses must register on the EmaraTax platform and apply for a Tax Registration Number (TRN) .

- Provide Required Information: When registering, businesses must provide information regarding their legal structure, trade name, business activities, and ownership.

- Submission of Essential Documents : Documents may include trade licenses, identification of authorized signatories, and proof of business activities.

Free Zone Entities Obligations Regarding Filing and Reporting

Once registered, Free Zone entities have the following filing and reporting obligations:

- Annual Tax Returns : Free Zone companies are expected to file corporate tax returns yearly showing their income and expenses.

- Consolidated Tax Return: They can file a single consolidated tax return instead of several returns for the different branches or entities.

- Compliance with Regulations : Businesses must adhere to economic substance regulations and transfer pricing rules.

Freezone Corporate Tax Filing Documents

Freezone Corporate tax in the UAE is calculated based on the net profit reflected in the company's financial accounts. To file tax returns and determine the amount of Corporate Tax owed, maintaining specific financial documents is essential. Here are the documents needed to prepare for filing Corporate Tax in the UAE:

- Financial statements for taxable income and exempt income calculation.

- Receipts for deduction claims.

- Records of asset depreciation for tax purposes.

- Documentation on transfer pricing and related party transactions.

- Information on financial reserve changes affecting taxable income.

- Proof of exemption status.

- Business loan documents for interest paid.

- Records of foreign taxes paid.

Free zone Corporate Tax Filing Timeline

Corporations and businesses operating in UAE freezones must adhere to specific deadlines for filing Corporate Tax . Here is a detailed timeline to help ensure compliance:

| Task | Description | Deadline |

|---|---|---|

| Tax Registration | Register with the Federal Tax Authority (FTA) for Corporate Tax. | Within 30 days of commencing business activities. |

| Tax Return Submission | Submit the annual Corporate Tax Return to the FTA. | Within 9 months from the end of the financial year. |

| Tax Payment | Settle the payable Corporate Tax amount. | Within 9 months from the end of the financial year |

| Deregistration | Submit a deregistration application if the business ceases operations. | Within 30 days of ceasing business activities. |

| Voluntary Disclosure | Submit a voluntary disclosure for any errors in the Tax Return or Tax Assessment | As soon as the error is discovered, preferably before notification of a Tax Audit |

| Declaration Submission | Submit any required declarations to the FTA | As specified by the FTA, usually within the same timeframe as the Tax Return |

| Notification of Change | Inform the FTA of any changes requiring amendments to tax record information. | Within 20 business days of the change occurring |

Penalties for the Free Zone Corporate Tax

The UAE currently doesn't impose specific penalties related solely to the Free Zone corporate tax regime. However, the general UAE freezone corporate tax framework outlines penalties for non-compliance that apply to both mainland and free zone businesses. Here's what you need to be aware of:

| No. | Description of Violation | Administrative Penalty Amount in AED |

|---|---|---|

| 1 | Failure to keep required records and other information specified in the Tax Procedures Law and Corporate Tax Law. | 10,000 for each violation; 20,000 for repeated violations within 24 months. |

| 2 | Failure to submit tax-related data, records, and documents in Arabic to the Authority when requested. | 5,000 |

| 3 | Failure to submit a deregistration application in the allowed period. | 1,000 monthly, up to 10,000 |

| 4 | Failure to inform the Authority of changes requiring amendment of tax record information. | 1,000 monthly, up to 10,000 |

| 5 | Failure of the Legal Representative to notify the Authority of their appointment within the specified timeframes. | 1,000 |

| 6 | Failure of the Legal Representative to file a Tax Return within the specified timeframes. | 500 monthly for the first 12 months; 1,000 monthly thereafter. |

| 7 | Failure of the Registrant to submit a Tax Return within the specified timeframe. | 500 monthly for the first 12 months; 1,000 monthly thereafter. |

| 8 | Failure to settle the Payable Tax. | 14% per annum on the unsettled amount, calculated monthly. |

| 9 | Submission of an incorrect Tax Return. | 500, unless corrected before the deadline. |

| 10 | Submission of a Voluntary Disclosure for errors in the Tax Return or Tax Assessment. | 1% monthly on the Tax Difference, from the due date until the disclosure is submitted. |

| 11 | Failure to submit a Voluntary Disclosure for errors before notification of a Tax Audit. | 15% fixed penalty on the Tax Difference; 1% monthly on the Tax Difference. |

| 12 | Failure to facilitate the Tax Auditor during a Tax Audit. | 20,000 |

| 13 | Late submission or failure to submit a Declaration to the Authority. | 500 monthly for the first 12 months; 1,000 monthly thereafter. |

How Corporate Tax Benefits for Free Zone Businesses

Free Zone businesses are to gain substantially from the corporate tax regime in the UAE:

- 0% Corporate Tax Rate: Qualifying income that arises from eligible activities shall be subject to a rate of 0% if the entity meets all regulatory requirements.

- Tax Incentives: The regime continues to respect the existing incentives for Free Zone businesses not undertaking mainland activities.

- Flexibility in Filing: The self-assessment principle allows businesses to manage their tax affairs proactively while ensuring compliance with local laws.

Reyson Badger - Freezone Corporate Tax Consultant

Freezone Corporate Tax in UAE can be tricky but it’s important to get it right. Filing your taxes on time and correctly helps avoid penalties and keeps your business running smoothly. Reyson Badger’s team is here to help you with every step, making sure you meet all the rules and requirements. With our full guidance , you can focus on growing your business while we handle your tax needs. Trust Reyson Badger to keep your tax matters in order, so you can achieve your business goals without any worries.

Latest Blogs

22

Jan

Accounts Outsourcing Services in Dubai: What Every Business Owner Should Know

Accounts Outsourcing Services in Dubai cover essential finance functions through a structured and professional workflow, compliant, and financially organized.

READ MORE →

19

Jan

VAT Impact on Company Profit in UAE: Key Factors Businesses Must Understand

Explore how VAT impacts company profit in the UAE, including compliance costs, pricing strategies, and the role of professional VAT services for businesses.

READ MORE →

19

Jan

Understanding VAT Refund Rules for Tourists in UAE Under FTA Guidelines

This guide explains VAT refund rules for tourists in the UAE, including eligibility, qualifying purchases, refund process, and key FTA guidelines to claim VAT refund in UAE.

READ MORE →

22

Jan

Why AML Checks Are More Important Than Ever in 2026?

Learn why AML compliance is vital in 2026. Avoid fines, protect your business, and meet new regulatory standards with strong AML checks.

READ MORE →

23

Jan

VAT Registration Threshold in UAE: Requirements, Calculation, and Compliance

READ MORE →

22

Jan

Amendment of the United Arab Emirates (UAE) VAT Decree-Law from 1st January 2026

UAE VAT Decree-Law amendments effective 2026 explained, including reverse charge updates, refund time limits, and enhanced FTA authority.

READ MORE →

19

Jan

Accounting Services in Dubai: A Practical Guide for Growing Companies

Accounting services in UAE, businesses gain clarity, confidence, and control over their finances allowing them to focus on what matters most: building and scaling their business in the UAE's competitive market.

READ MORE →

23

Jan

Corporate Tax Advance Pricing Agreements in the UAE

Advance Pricing Agreements (APAs) in the UAE help businesses obtain certainty on transfer pricing methods under the Corporate Tax regime. Learn how APAs work, eligibility criteria, benefits, and compliance requirements set by the UAE Federal Tax Authority

READ MORE →

23

Jan

UAE FTA Moves to Free Digital Tax Certificates: What It Means for Businesses?

The UAE FTA now offers free digital tax registration certificates with QR codes, eliminating paper fees and simplifying compliance for businesses.

READ MORE →

21

Jan

UAE FTA Removes Fees for Paper Tax Certificates, Moves to Free Digital Certificates

UAE Federal Tax Authority removes fees for paper tax certificates and introduces free digital certificates with QR codes from January 2026.

READ MORE →