The VAT registration threshold in the UAE specifies the turnover level at which businesses must register for Value Added Tax with the Federal Tax Authority. Non-compliance results in substantial fines, operational interruptions, and legal sanctions. Under Federal Decree-Law No. 8 of 2017 on Value Added Tax and its subsequent amendments (including Decree-Law No. 16 of 2025), entities exceeding the threshold face clear regulatory obligations. This document details the UAE VAT threshold, including its calculation, mandatory and voluntary registration rules, and key compliance measures to help business owners avoid penalties and ensure alignment with FTA requirements.

What is the VAT Registration Threshold in the UAE?

The VAT registration threshold is the turnover limit requiring businesses to register for VAT with the Federal Tax Authority. This threshold serves as a crucial compliance benchmark for both new and existing businesses in the UAE. Two separate thresholds apply under the UAE VAT system: the mandatory threshold and the voluntary threshold, each with specific eligibility and compliance implications.

Correctly identifying this threshold is essential for tax compliance and business continuity. When a company’s taxable turnover meets or exceeds the set figure, VAT registration becomes compulsory. Failure to register on time can lead to financial penalties and damage to business reputation. Businesses must understand the turnover definition and maintain the required documentation to mitigate regulatory risk and streamline operations.

Mandatory Threshold: When VAT Registration Is Required

The UAE enforces a strict VAT registration threshold requiring businesses to register when their taxable supplies and imports exceed AED 375,000 within the previous 12 months or are expected to exceed this amount within the next 30 days. This applies to both mainland companies and designated free zone entities engaged in the local economy. Timely registration is critical to avoid penalties and safeguard business credibility. Non-compliance carries significant operational and financial consequences. Refer to FTA regulations and current compliance guidelines for comprehensive eligibility and business classifications.

Definition of Mandatory VAT Registration Threshold

The mandatory VAT registration threshold triggers when a business’s annual taxable turnover or projected supplies reach at least AED 375,000. Businesses meeting this criterion must apply to the Federal Tax Authority without delay. Failure to register promptly may result in administrative fines and further regulatory sanctions. Continuous monitoring of turnover components enables businesses to comply proactively with FTA deadlines and avoid penalties. Entities should review official guidance for specific thresholds, considering sector-specific and cross-border transaction factors.

What Counts as Taxable Supplies?

Different supply types affect the threshold assessment and VAT registration eligibility. Accurate classification of revenue streams is essential to ensure compliance.

- Standard-rated supplies subject to 5% VAT: Supplies taxed at the standard rate must be included in turnover calculations.

- Zero-rated supplies included in turnover calculation : Supplies taxed at 0% VAT count towards the threshold.

- Exempt supplies excluded from threshold calculation : Revenues from exempt supplies are excluded when assessing the threshold.

Application to Mainland and Free Zone Businesses

Both UAE mainland and qualifying free zone businesses must register for VAT if their taxable turnover meets or exceeds AED 375,000. For free zones, only entities conducting business within the local market are subject to this obligation, including those in Designated Zones, as they are considered within the UAE for VAT purposes, except for specific supplies of goods. It is necessary to aggregate taxable supplies across all operational branches and group entities to ensure compliance. Reviewing the FTA’s rules on business establishment and principal place of business clarifies special circumstances affecting mainland and free zone entities. Refer to guidance such as the Eligibility Criteria for VAT Registration UAE and Who Should Register for VAT in UAE? for detailed information.

Voluntary VAT Registration Threshold

The voluntary VAT registration threshold allows smaller businesses and startups to register for VAT before reaching the mandatory turnover limit. Businesses with annual taxable turnover exceeding AED 187,500 but below the mandatory threshold may voluntarily register with the Federal Tax Authority. This enables SMEs and new companies to recover input VAT and strengthen credibility with clients and suppliers.

Voluntary registration is a strategic decision for companies aiming to build their brand, facilitate cross-border operations, or prepare for growth. However, voluntary registrants must comply with the same VAT operational standards as mandatory registrants. For sector-specific information, consult resources such as VAT Registration for Startups in Dubai.

Voluntary Registration Threshold Explanation

The voluntary threshold is set at AED 187,500 of taxable turnover over the past 12 months or expected in the next 30 days. Registration below the mandatory threshold enables compliance with VAT regulations and access to input VAT recovery. Following voluntary registration, businesses must submit VAT returns and maintain adequate tax records. This threshold supports startups and SMEs to compete effectively in the regulated market.

- Applies to businesses with turnover below the mandatory threshold but above AED 187,500.

- Once registered, businesses must comply fully with VAT regulations and filing requirements.

- Benefits include improved credibility and access to VAT recovery, useful for startups and SMEs.

Benefits of Voluntary VAT Registration

Voluntary VAT registration provides significant benefits. Registrants can reclaim input VAT on expenses, improving cash flow and lowering tax liability. It also demonstrates financial reliability and professionalism, strengthening relationships with clients and partners. Additionally, a VAT registration number facilitates smoother cross-border transactions and international invoicing. Businesses must understand their regulatory responsibilities to maximize these operational and reputational advantages.

Situations Favoring Voluntary Registration

Certain business models benefit from voluntary VAT registration. Companies with substantial input costs, startups building market presence, and organizations dealing with VAT-registered clients gain operational and financial efficiencies by registering early.

- Businesses with large input purchases are aiming to reclaim VAT and enhance cost efficiency.

- Startups seeking to establish professional credibility for market entry or investment.

- Companies working with VAT-registered clients who require VAT invoices to facilitate transactions.

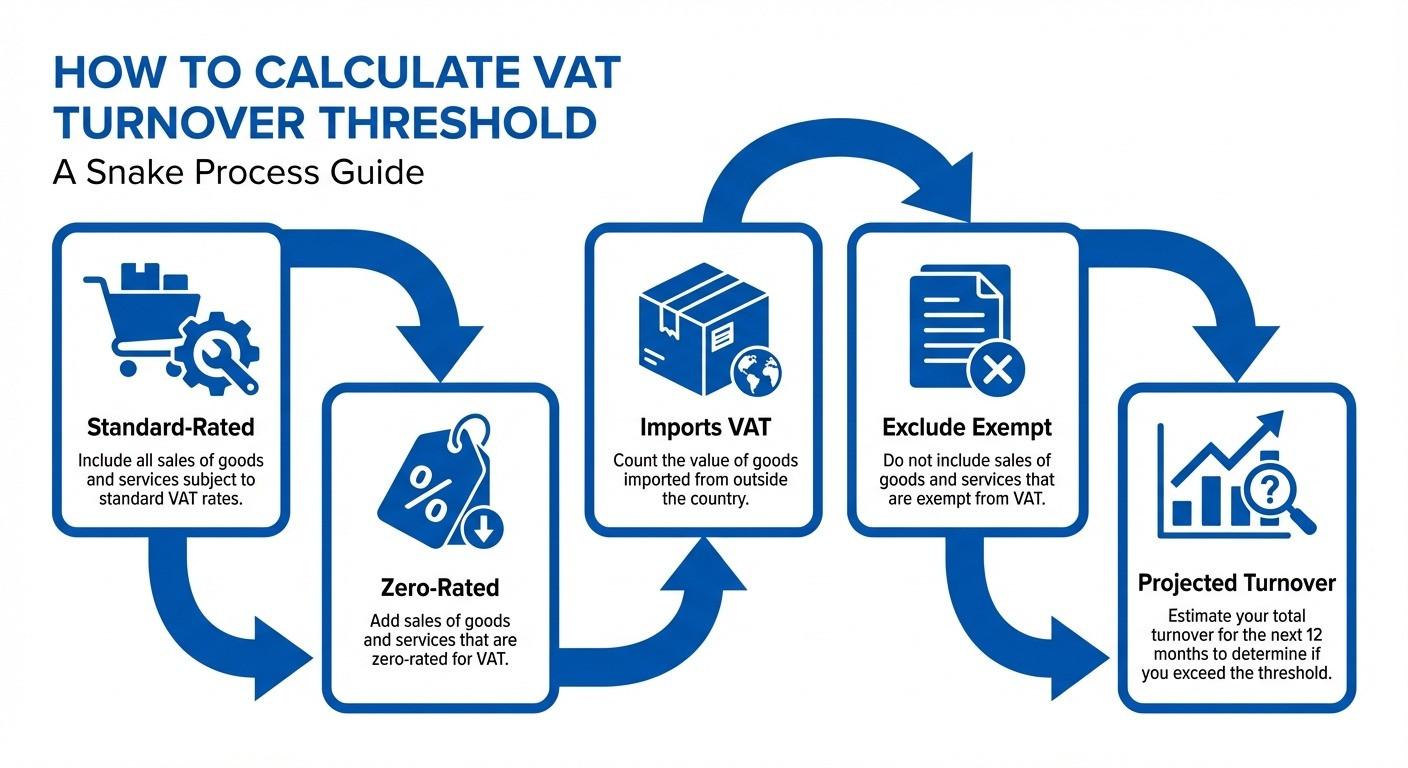

How to Calculate VAT Turnover Threshold (Step-by-Step)

Calculating the VAT registration threshold requires precise identification and classification of business supplies. Companies must assess taxable turnover over a continuous 12-month period and forecast anticipated revenue over the next 30 days to comply with both retrospective and prospective criteria. Only taxable supplies, imports, and reverse charge items qualify; exempt supplies and non-business income must be excluded. Errors in calculation risk FTA penalties and audit exposure. Multi-entity organizations must accurately aggregate turnover across branches and subsidiaries.

Special focus on the treatment of standard-rated, zero-rated, and exempt supplies, as detailed in UAE VAT: Standard, Zero-Rated, and Exempt Supplies, is essential to avoid miscalculations that distort compliance status.

Identify Taxable Supplies to Include

Turnover calculation must incorporate all taxable supplies. This includes standard-rated and zero-rated goods and services, as well as imports subject to VAT and supplies under the reverse charge mechanism.

- Standard-rated goods and services are the main turnover components.

- Zero-rated supplies are counted despite their 0% VAT rate.

- Imports subject to VAT, paid at customs, are added to the taxable turnover.

- Reverse charge supplies, such as certain cross-border services, are included.

Supplies and Activities to Exclude

Exempt supplies and non-business revenue must be distinctly excluded from turnover calculations. This includes exempt financial services, sales of bare land, and local passenger transport services. Also, exclude non-economic receipts, such as capital injections, grants, or private transactions. Maintaining this distinction avoids overstating or understating taxable turnover.

Example Scenarios of Turnover Calculation

Examples clarify turnover aggregation for VAT registration. A service company with AED 250,000 turnover composed of both zero-rated and standard-rated supplies must include both when evaluating registration status. Mixed suppliers handling taxable and exempt goods must aggregate only taxable supplies while excluding exempt revenues. Companies with multiple operational lines should total all qualifying supplies across divisions.

- A company with AED 250,000 turnover, including zero-rated supplies, calculates the full taxable turnover for registration decisions.

- A mixed supplier combines standard-rated and zero-rated sales but excludes exempt supplies from calculation.

Considering Projected Turnover for Early Registration

The FTA requires immediate VAT registration if projected taxable turnover for the next 30 days exceeds AED 375,000. Businesses experiencing rapid growth or seasonality must monitor forecasts and register promptly to prevent violations. Early registration prevents inadvertent breaches during expansion or new contract acquisition. Reliable forecasting combined with vigilant record-keeping is critical for timely compliance.

Common Mistakes & Compliance Tips for VAT Threshold Calculation

Errors in VAT threshold calculations frequently prompt FTA investigations, cause operational setbacks, and result in fines for late or inaccurate registration. Common mistakes include mixing zero-rated with exempt supplies, misclassifying revenue, and failing to review turnover regularly. Minimizing these risks requires scheduled reviews, expert consultation, and adopting suitable accounting systems. Maintaining comprehensive documentation and monitoring regulatory updates is essential for sustained compliance. Refer to Top VAT Filing Mistakes UAE Businesses Should Avoid, Tips for Avoiding VAT Penalties for Business in the UAE, and VAT penalty guidance for further details.

1. Mistake: Confusing Zero-Rated vs Exempt Supplies

Confusing zero-rated with exempt supplies leads to inaccurate threshold calculations. Zero-rated supplies count towards turnover and permit input VAT recovery, whereas exempt supplies do not count towards registration thresholds. Misclassification can result in underreporting or overreporting, triggering FTA audits and fines.

- Zero-rated supplies must be included in turnover calculations.

- Exempt supplies are excluded and do not require VAT registration.

- Misclassification leads to inaccurate reporting and compliance risks.

2. Mistake: Including Non-Taxable Revenues Incorrectly

Including exempt activities or non-business revenues improperly inflates taxable turnover, causing erroneous registration and complications. Examples include private income, donations, or capital injections. Only economic activities subject to VAT should be considered to avoid registration errors and penalties.

3. Mistake: Failing to Monitor Turnover Frequently

Neglecting regular turnover monitoring often results in missed registration deadlines and avoidable fines. Businesses must conduct monthly or quarterly turnover reviews, utilize accounting software for accuracy, and seek tax professional advice to maintain compliance.

- Regular monthly or quarterly turnover assessments are essential.

- Accounting tools help track taxable supplies and reduce errors.

- Tax advisors provide strategic VAT compliance planning and documentation oversight.

Compliance Tips for Accurate VAT Registration

Adopting best practices such as updating records promptly, reassessing registration eligibility periodically, and engaging professional advisors—supports accurate VAT registration. Staff training, subscription to FTA updates, and internal VAT audits further reduce compliance risks and prevent penalties.

Adopting best practices such as updating records promptly, reassessing registration eligibility periodically, and engaging professional advisors supports accurate VAT registration. Staff training, subscription to FTA updates, and internal VAT audits further reduce compliance risks and prevent penalties.

Conclusion

Correctly interpreting and applying the VAT registration threshold is essential for sustainable business operations in the UAE. Maintaining accurate records and actively monitoring turnover ensures timely registration, optimal input VAT recovery, and avoidance of financial and reputational consequences associated with late filings and penalties. Partnering with an experienced advisor ensures full compliance with FTA mandates while allowing businesses to focus on strategic growth. Entrusting Reyson Badger delivers expert guidance, regulatory insight, and timely execution that support sustained compliance with evolving VAT regulations in the UAE.

Frequently Asked Questions (FAQs)

1. What is the current mandatory VAT registration threshold in the UAE?

The mandatory threshold is AED 375,000 in taxable supplies within the past 12 months or expected in the next 30 days, as stipulated under the VAT Law.

2. What supplies must be included when calculating the VAT registration threshold?

The calculation must include standard-rated supplies, zero-rated supplies, imports subject to VAT, and supplies subject to the reverse charge. Exempt supplies and non-business income are excluded.

3. What are the benefits of voluntary VAT registration in the UAE?

Voluntary registration enables input VAT recovery, enhances business credibility with clients and partners, and facilitates smoother cross-border transactions.

4. How often should businesses monitor turnover for VAT registration?

Businesses should perform turnover reviews at least monthly or quarterly to ensure timely registration and prevent penalties.

5. What penalties apply for late VAT registration in the UAE?

Late registration incurs a fixed administrative penalty of AED 10,000, accompanied by further sanctions from the FTA.